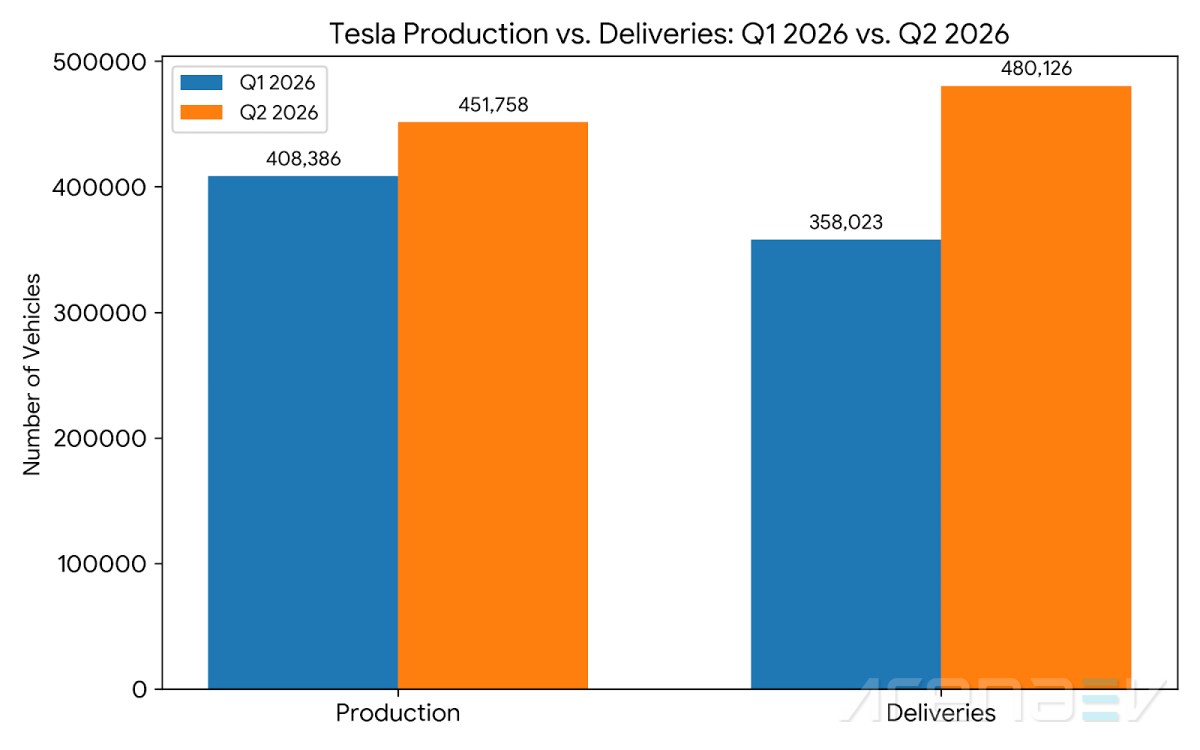

Tesla revitalized its sales figures in Q2 2026, marking a significant turnaround. The American automaker delivered 480,126 electric vehicles globally from April to June, reflecting a 25% increase compared to the same quarter in 2025, when it delivered 384,122 vehicles. The volume also surged by 34% from the 358,023 units delivered in Q1 2026.

Unlike previous quarters where production outpaced consumer demand, Tesla effectively managed its inventory this time. The company produced 451,758 vehicles in Q2 and delivered 28,368 more cars than it manufactured. This enabled Tesla to significantly reduce the unsold inventory that had accumulated earlier in the year. In Q1 2026, Tesla produced 408,386 vehicles but sold only 358,023, resulting in a backlog of 50,363 units.

The delivery figures surprised industry analysts, who had projected lower numbers. The Wall Street consensus estimated 406,024 deliveries, while Bloomberg offered an even more conservative prediction of 396,465 vehicles. Even the most optimistic forecasts, such as Goldman Sachs at 420,000 and Barclays at 418,000, fell short of Tesla's actual performance by over 60,000 units, leaving little room for skepticism among analysts.

High-demand models, specifically the Model 3 sedan and Model Y crossover, were the driving force behind these numbers, accounting for 442,936 vehicles produced and 467,762 vehicles delivered. Tesla's niche lineup, including the Model S, Model X, Cybertruck, and Semi truck, contributed 8,822 units to production and 12,364 to global deliveries.

Despite achieving the most successful second quarter in its history, Tesla did not break its all-time record. That record remains with Q3 2025, when deliveries peaked at 497,099 units, influenced largely by an influx of buyers eager to claim the $7,500 federal tax credit before it expired on September 30, 2025.

The loss of this tax credit affected local demand in North America. Ahead of the Q2 report, Cox Automotive anticipated a substantial 20% year-over-year decline in U.S. sales, which would reduce Tesla's market share in the U.S. to about 2.9%. However, international factors largely mitigated these domestic challenges, as a war in Iran drove global gasoline prices up, causing many international buyers to switch from traditional combustion vehicles to electric ones.

International markets, particularly in China and various European regions, absorbed the surplus inventory effectively. In China, Tesla's wholesale deliveries reached 254,551 vehicles, representing a 33% year-over-year increase, with June contributions alone accounting for 89,091 units of locally produced Model 3 and Model Y variants. Europe also demonstrated a robust recovery, with new registrations more than doubling in France, increasing by 56% in Sweden, and rising by 39% in Denmark during June.

This global growth has narrowed the gap between Tesla and its main international rival, BYD. The Chinese automaker delivered 557,090 fully electric vehicles in Q2 2026, solidifying its position at the top of the global battery-electric vehicle market. Interestingly, while Tesla achieved a 25% increase, BYD's battery-electric vehicle deliveries fell by approximately 8% compared to the previous year. This has reduced Tesla's trailing gap from 220,000 units last year to around 77,000 units currently.

In addition to its automotive achievements, Tesla's energy storage division continued its steady growth. The company deployed 13.5 GWh of energy storage products this quarter, marking an increase of more than 50% compared to Q1 2026 and a 40% rise from the 9.6 GWh deployed in Q2 2025. Although this figure slightly fell short of the 13.8 GWh anticipated by internal trackers and independent analysts, energy storage remains the fastest-growing segment of Tesla's business.

Despite these impressive delivery results, the stock market reacted with the typical "sell-the-news" response, causing Tesla shares to drop by 7% to $395.86 in morning trading. Investors are wary of the company’s high valuation, with a forward price-to-earnings ratio of 204x and a trailing ratio of 421x, especially considering its modest 4% net margin.

Prediction platforms such as Polymarket had already calculated a 98% probability of a drop following the report. Shareholders appear to be looking beyond immediate vehicle delivery numbers, focusing instead on potential corporate changes following SpaceX's substantial initial public offering in June, alongside future projects like the Cybercab, Semi, and Optimus robotics initiatives.

Source